That night, like most nights, Phillip J. Cannella 3rd warned that the financial world was at the brink of a massive meltdown, one that would wipe out savings and crush retirees.

“We’re about to enter a horrible period, crash followed by recovery, followed by inflation,” the insurance agent said last fall, pacing excitedly in front of nearly 100 retirees and middle-aged guests at the Springfield Country Club, enticed by the promise of a free dinner.

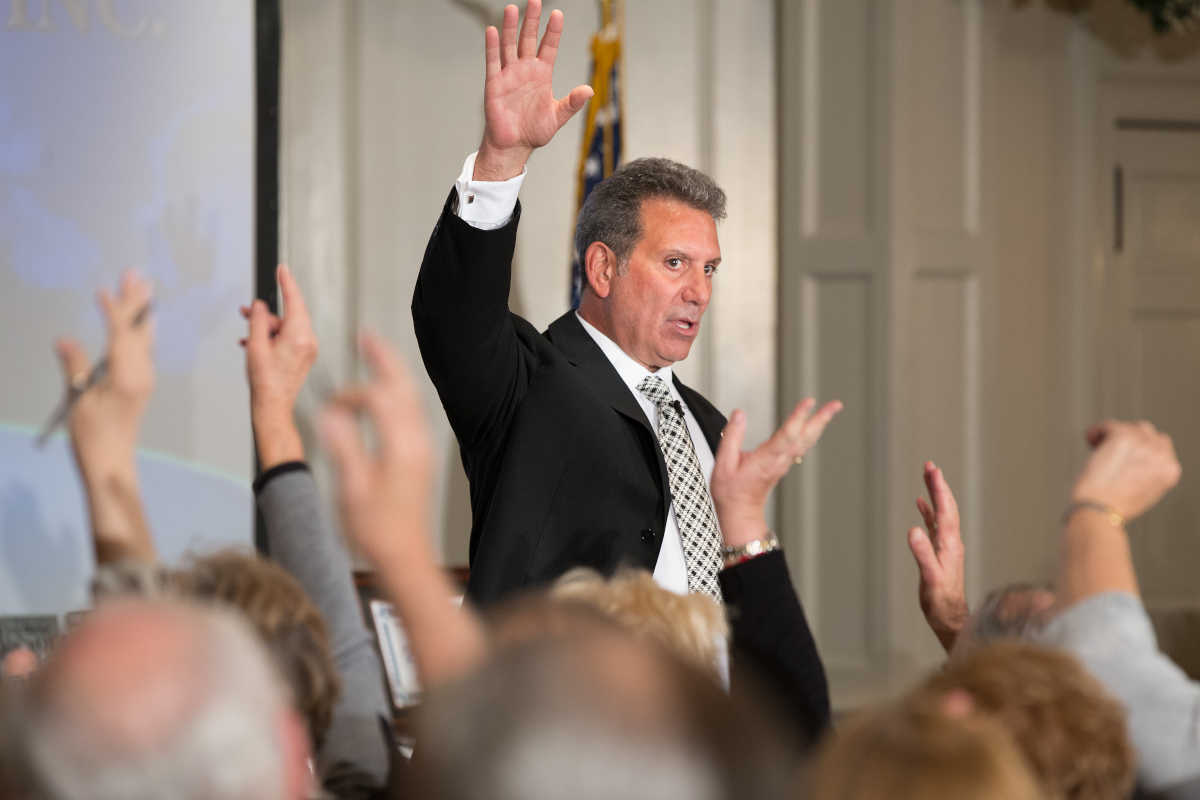

When he asked for a show of hands of who lost money in the 2008 financial crash, about half raised theirs. “It’s going to be a world collapse, economically speaking,” Cannella warned them. “You need to plan for this storm coming. You need to be in a vehicle that’s not going to sink when Wall Street sinks.”

If Wall Street is the problem, Cannella believes he has the solution: fixed index annuities, a popular but complex insurance product known for lucrative commissions and opaque fees.

Sales of these lightly regulated investments have surged since the 2008 financial crash, when mom-and-pop investors saw the stocks and mutual funds they counted on for retirement plummet in value. Seizing opportunity, insurance agents began pitching these annuities on cable TV and radio infomercials, telling seniors how to protect their savings with investments reassuringly described as “risk free” and “no fee.”JESSICA GRIFFIN / Staff PhotographerAt a free dinner to promote fixed index annuities, Phillip J. Cannella 3rd asks for a show of hands to illustrate how many lost money in the 2008 market crash. His spiel includes warnings of economic collapse, but he leaves out key information to prove his product is safer than stocks and mutual funds.

But in Pennsylvania and most states, sales agents aren’t required to disclose their commissions, typically 6 to 10 percent, that insurance carriers pay them for putting retirees’ money into these long-term investments. Seniors also can face huge penalties for early withdrawals for unexpected medical bills or other emergencies.

California Insurance Commissioner Dave Jones, who oversees the nation’s biggest insurance market, urged caution: “We’ve seen people being sold annuities that are entirely unsuitable because of their age, because of their financial circumstances. … It’s an area of increasing complexity, a population that is extremely vulnerable, and one in which there is a lot of room for mischief.”“It’s an area of increasing complexity, a population that is extremely vulnerable and one in which there is a lot of room for mischief.”Dave Jones, California Insurance Commissioner

The U.S. Department of Labor, which has oversight of retirement plans, became alarmed about insurance agents and investment brokers pushing clients into inappropriate retirement investments with high or undisclosed commissions. These practices, it estimated, cost retirees $17 billion a year in excess fees.

The department crafted a regulation, set to take effect in April, that would require financial advisers to put their clients’ interests first when selling investments for retirement. Known as the “fiduciary rule,” it was the first federal regulation of insurance agents, including some of the 230,000 in Pennsylvania.

With its potential for curtailing high-commission insurance sales, Cannella said, the rule was “going to knock out half” of the agents selling annuities.

But in February, President Trump, by an executive order, halted the long-debated regulatory change and called for another review. The insurance and investment industry had fought the new rule for years and hope the new administration can kill the Obama-era reform.

If so, sales of insurance products will remain overseen primarily by state regulators, unlike sales of stocks and mutual funds, which have some federal consumer protections.

In Pennsylvania, investors have poured billions of dollars into fixed index annuities over the last decade just as the state Insurance Department has been slashing its staff. It has 225 employees, slightly more than half its 2006 workforce of 414.

Fewer regulators for a growing market

The number of employees at the Pennsylvania Insurance Department fell from 414 in 2006 to 199 in 2016. As a rate per premiums sold, the state has fewer than half the regulators than the national average.Insurance department employees per $1 billion in premiums.

Meanwhile, staffers in the department who look into consumer complaints have been saddled with the highest annual caseloads in the nation. In 2014, each consumer staffer on average had 655 complaints — more than three times the national average, according to an Inquirer analysis of insurance-industry data. (Their New Jersey counterparts had a caseload of 163.)

Asked whether the department could keep up with its thousands of annual consumer complaints, spokesman Ronald G. Ruman said the agency has enough staff to be “fully able to do the job needed to enforce our laws and protect Pennsylvania consumers.”

Q: What is an annuity?

An annuity is a contract between you and an insurance company—a contract that promises to pay you a certain amount of money over a specified time. Social Security is one example of an annuity that pays retirees steady cash flow in retirement.

Typically, retirees who wish to guarantee a minimum income stream during their retirement years may purchase annuities.

Q: What should I look out for when buying an annuity?

Commissions & Fees

Agents typically reap commission of 6% or more, depending on the contract. So on a $100,000 annuity the agent makes $6,000. Annuities can lock up your money for a decade or longer, and if you cash out early, you may pay a “surrender charge” of between 10 to 22 percent. That means on a $100,000 annuity, if you cash out early, you could pay a penalty of $10,000 to $22,000, not including commissions. Surrender charges decline the longer you leave in your money.

Q: Who should buy an annuity?

For those who have no pension or want a supplement, annuities can provide income, help avoid overspending and provide a floor of guaranteed money. Annuities may be inappropriate or too expensive for people who have shorter-than-normal life expectancies. The elderly, who may not outlive these insurance contracts, should likely avoid annuities.Do-it-yourself retirement planning

Consumer protection for seniors has become all the more important because of a tectonic shift in how Americans prepare for their retirement. Today, old-standby pension plans – in which the employer provides a fixed monthly payout for life – are offered by only 5 percent of Fortune 500 companies, down from 50 percent in 1998, according to a recent study.

Retirement planning is now more do-it-yourself, with some turning to fixed index annuities. They’re marketed as a way to give investors a portion of the stock-market gains while protecting against market downturns. But they’re hard to understand for most investors. The “fixed” part of the annuity is this: The company will set a minimum rate of return on money invested, often about 1 to 2 percent a year over the term of the contract, often six to 17 years.

The “index” part is tied to the S&P 500 or another well-known market index, and can provide an upswing of several more percentage points, depending on how the stock market performs. But the insurance company typically caps how much of the upswings an investor receives.

For those who find comfort in a minimum guaranteed return, even if small, and strict control on their money, some experts say putting a portion of savings in index annuities can be a good choice. But Barbara Roper, director of investor protection at the nonprofit Consumer Federation of America, said “absent real reforms … just stay away.”“A magical mutual fund”

Cannella, 61, founder of the King of Prussia-based First Senior Financial Group, is something of a local celebrity. He hosts an hour-long paid radio infomercial every Saturday and Sunday on 1210 AM, the Philadelphia affiliate of CBS. He says he spends as much as $2 million a year on advertising, a lot of it airing on cable TV news shows. His company, headed by his wife, Joann Small, writes $100 million in contracts annually taking in $6 million to $8 million in commissions, he said. He also is licensed to sell insurance in Florida.JESSICA GRIFFIN / Staff PhotographerAt his events, Phillip J. Cannella portrays himself as a lone, fearless advocate for seniors, unafraid to reveal harsh truths about Wall Street. Stock brokers compete with insurance agents for retirees’ money.

“I am the expert on fixed index annuities. No one knows more because I’ve taken the time to care and learn,” he said. But he doesn’t call them annuities at his presentations. He prefers to describe them as “crash-proof” investments, “like a magical mutual fund.”“I am the expert on fixed index annuities. No one knows more because I’ve taken the time to care and learn”Phillip Cannella

He portrays himself as a lone, fearless advocate for seniors, unafraid to reveal harsh truths about Wall Street, willing to sacrifice everything to its counterattacks. Stock brokers compete with insurance agents for retirement investments, and Cannella criticizes them. But his characterizations are harsh: greedy, corrupt, the enemy. As a result, he said in an interview, his competitors are responsible for numerous complaints against him with state regulators. (The state Insurance Department doesn’t reveal or discuss consumer complaints. In contrast, consumer complaints about stockbrokers are publicly searchable in the national BrokerCheck database.)“Wall Street wants control of fixed index annuities”https://www.youtube.com/embed/QrxqAlmcbDE?rel=0&controls=0&showinfo=0

Some of his clients, Cannella said, are even worried that he’s putting himself in harm’s way for exposing “the atrocities on Wall Street.”

“If I get picked off for doing something great nationally, I’m OK with that,” he said. “Isn’t that how Martin Luther King died? They all died for a cause, and the cause still survives. … So, I’m not afraid to die.”

What is important to understand, he said, is that his product is safer than stocks and can earn bigger returns. At the Springfield Country Club last fall, he showed the crowd a version of a promotional chart that insurance agents across the country use to push fixed index annuities. Annuities, Cannella told his audience, out-performed the stock market “every year.”

The chart, by industry giant American Equity Investment Life Insurance Co., shows one of its fixed index annuities outperforming the S&P 500 index from 1998 to 2015. But there was a major omission:

What Cannella and other agents don’t mention is the S&P 500 returns on the chart do not include reinvested dividends. With dividends included, the stock market’s aggregate return handily outperformed Cannella’s favorite annuity product over the same period.

How they sell you…

Like thousands of insurance agents across the country, Phillip Cannella 3rd, one of the region’s leading promoters of fixed-index annuities, used a version of this chart in his sales presentations to show that investing in annuities is safer than the stock market. The chart showed that $100,000 invested in 1998 in an annuity offered by American Equity Life Insurance Company outperformed the nominal S&P 500, a broad-based stock market index.

Asked later why he used a chart without telling his audience that stock dividends aren’t included, Cannella said he was using insurance company marketing material, all of which is approved by the Pennsylvania Insurance Department. Ruman, the department spokesman, said promotional materials get vetted and approved if the agency has received a complaint about them. He couldn’t confirm whether the department received a complaint about such a chart.

Cannella also said customers of First Senior Financial are protected because insurance agents are held to a higher standard than Wall Street demands.

“Licensed professionals in our insurance industry must operate under a fiduciary duty,” he said in an interview. “There is no fiduciary duty with Wall Street.”

Questions to ask before you buy a fixed index annuity

When do I want the income to start?

What are the A.M. Best and other financial strength ratings of the insurance company?

For how long after I receive my annuity contract can I cancel for a full refund?

What charges, if any, are deducted from my premium & when?

What charges, if any, are deducted from my contract value & when?

What are the surrender charges if I want to take out all of my money?

For how many years will the surrender charges apply?

Can I get a partial withdrawal without paying charges or losing interest?

What are the risks that my annuity/earned interest could decline in value?

Is there a guaranteed minimum interest rate?

How will my annuity income be taxed?

What happens to my account balance and income payments if I die?

Under federal law, only Registered Investment Advisers, who typically charge clients hourly fees for advice and file annual compliance documents with the federal Securities and Exchange Commission, have a fiduciary duty — putting a client’s interest ahead of earning a bigger commission. Cannella does not have to offer the best deal for consumers; his obligation is to sell products that are “suitable” for the consumer. The suitability standard varies state to state. In contrast, stockbrokers are governed by a national standard.

Roper of the Consumer Federation of America says “suitable” is a low standard for the financial industry. In her view, it offers the public little protection. “Suitability lets you recommend the worst of all suitable options,” she said.

“The seller remains free to recommend the one most profitable to him or her, rather than the one best for you.”Fans and critics

Cannella has critics dating to the 1990s — when the Pennsylvania Insurance Department fined him $10,000 and suspended his license for three months. It accused him of improper sales of health insurance policies to the elderly. The department said he had been involved in “misrepresenting the benefits and coverage of the policies being sold” and selling “duplicate coverage to persons in excess of 60 years of age.”

Cannella said the case was ginned up by his competitors and was unsubstantiated. He said he paid the fine and accepted the suspension without admitting wrongdoing because he was a young insurance agent, supporting a family, and was financially unable to face a drawn-out court battle.

Cannella’s brother-in-law, who worked for him for about a year, once described the company’s sales tactics at its senior seminars.

“The theme was very consistently gloom and doom, and the market is going to crash and bad things are going to happen,” Stephen M. Fine, after he left the company, said in a deposition filed in a lawsuit First Senior brought against a former accountant. “Wall Street is bad and everything about Wall Street is bad and only we’re good.”“We want to make sure that we leave the least amount of money on the table and we get — garner back the highest commissions to us”Stephen M. Fine

Fine said the company sought to invest as much of the clients’ money as possible. “We want to make sure that we leave the least amount of money on the table and we get — garner back the highest commissions to us,” Fine said.

In an interview, Cannella disputed that his firm put the totality of its clients’ savings in annuities. He provided account statements for a dozen clients that showed his company invested no more than 80 percent in annuities. As for his brother-in-law, Cannella said he fired him and disputes his account.

More recently, the family of Delaware County resident Kay Guzman, 68 at the time, complained she was inappropriately persuaded to cash out a long-held $1 million insurance policy to buy fixed index annuities. When Guzman realized the mistake, she said in court records, she couldn’t get a new life insurance policy because she was a cancer survivor. She sued Cannella, First Senior, and others.

Cannella said competitors may have convinced Guzman she could make money by filing suit. Both parties said they expect to settle soon.“I did a billion with no complaints, no lawsuits… that’s almost like walking on water.”https://www.youtube.com/embed/nKBCECZ2FIM?rel=0&controls=0&showinfo=0

Cannella does have many clients who swear by him. Stephen Desirey, 69, of Schwenksville, and his wife are satisfied with the fixed index annuities they purchased. “If an individual is looking for a safe place to hold extra retirement funds that they believe will not be needed until after the next 10 years, they are terrific vs. the alternative risk,” he said in an interview.

Some claims on Cannella’s website raise questions. Cannella says many of his clients got “double-digit returns” on their investments with First Senior. Below the photo of John J. Wallin, now 83, a retired Philadelphia Electric manager, the text read: “8.3% 1 YEAR AVG.”

Stealing retirement

The Nave sisters were victims of annuities salesman Richard Piccinini Jr., who pocketed nearly $200,000 from their $500,000 retirement savings by moving them through dozens of complicated, commission-rich insurance contracts.How Annuities Can Drain Seniors’ SavingsCourtesy of the Nave family

Wallin, of Chester County, said he never earned anything near 8.3 percent since he put $300,000 in the annuity in 2014. He’s gotten 4 to 5 percent a year, a return he’s happy with.

The difference appears to be in the way Cannella’s firm calculates the returns. Wallin’s 10-year contract came with a 10 percent first-year bonus from the insurance company. Cannella said his company includes the one-time bonus to help investors “get out of the gate” and his figures are accurate.

Wallin’s fixed index annuity matures when he’s 90 but will be transferred without penalty to his wife if he dies before then. More important, he said, none of the principal will be lost if the stock market drops.

A photo of John Vitko, who invested in a 15-year contract in 2013, appears above the words “6.2% 2 Year Avg.”

Vitko, 66, a former salesman in Northeast Philadelphia, said he made 1.5 percent in interest the first year for one annuity, then about 1 percent for a while, and 1.75 percent last year. He said Cannella’s firm added some of the bonus to come up with the 6.2 percent figure. “It’s really not all earnings,” he said.

Some content on this page was disabled on June 11, 2020 as a result of a DMCA takedown notice from Philadelphia Inquirer. You can learn more about the DMCA here:

A Main Line Philadelphia start-up wants to manufacture America’s first-ever “smart gun,” a 9-millimeter pistol that uses radio-frequency ID technology to provide a layer of safety for police officers and eventually American consumers, the world’s biggest gun buyers.

For the last two months, LodeStar Firearms has been seeking to raise $5 million to design and make a product that its backers say could prevent thousands of shootings a year and sharply curtail gun thefts. It aims to sell more than a million guns annually in five to seven years.

That would be a huge achievement for the fledgling firm since no one has yet sold a single smart gun on these shores. Smart guns have faced enormous blowback from the National Rifle Association, which rejects the technology as costly, unreliable, and an expansion of government control over firearms. Opponents have blocked sales of smart guns, leading other start-ups like the German weapon-locks firm Armatix to go bankrupt trying.

LodeStar CEO Gareth Glaser didn’t start out as a gun guy. The former tax lawyer and University of Pennsylvania graduate worked in corporate America for most of his career at ExxonMobil and Alcon, the eye-care unit of Novartis. But in 2017, he took part in a Harvard graduate school project, encouraging experienced executives to take on social problems, and came to believe that “smart guns” represented an untapped business opportunity.

“I did some research and found that, like auto accidents, safety with guns can be increased by technology like seat belts and air bags in cars,” Glaser said at his Radnor home, which doubles as LodeStar’s headquarters. The firm is banking on consumers’ willingness to use “smart” recognition technology in their daily lives, including phones that open to your face, cars that start to a driver’s voice, and television remotes that search for movies from simple commands.

Invited to speak on a smart-gun technology panel in 2017, Glaser met the legendary German gun designer Ernst Mauch, chief designer for Heckler & Koch. Most aficionados recognize H&K as the premier weapons maker for police and the military. Mauch developed the MP-5 submachine gun and other guns widely used by SWAT teams, federal law enforcement, customs, and border patrol.

Mauch is retired, and still keen on designing a smart gun, so he became LodeStar’s chief gun designer. “He has the design background, and I had the business experience,” Glaser said, explaining LodeStar’s birth.

Mauch and his team of German engineers are working on a 9mm prototype to exacting specifications, with the hope that they will have a Glock-style weapon for sale sometime in late 2018 or early 2019. The price would be in the $700-to-$800 range, including two hours of training with a firearms instructor.

The firm wants to put smart-gun manufacturing in the U.S., Glaser said. “Smart guns are a small niche business right now, but there are really no competitors. If our smartphones can recognize our fingerprints or our faces, why can’t guns?”

Why? To date, traditional manufacturers have expressed distrust of the technology as have many gun owners, fearing that the guns could malfunction or fail to fire during a mud-filled confrontation.

Those views “will likely change, just as it has with Detroit and self-driving cars,” maintained Michael Farrell, a LodeStar board member and weapons trainer. Farrell founded Smart Firearms, a Tempe, Ariz.-based company training leading law enforcement agencies including the Phoenix, D.C. Metro, Boston, New York Police Departments and the New York Department of Corrections.

“When Ernst Mauch joined LodeStar, that sealed it for me,” said Farrell.

The U.S. firearms market totals $7 billion a year, or roughly 12 million guns. And Americans already own roughly 300 million out of the 650 million guns in circulation globally.

“We buy half of all the world’s guns, so the average American gun owner buys eight or nine weapons, and 40 percent of those people keep one gun loaded” in their house, said Glaser.

“We want the loaded gun to be our smart gun,” he said, describing the firm’s market. Today, a smart gun will compete with traditional handguns made by Glock, the maker of pistols used by over 65 percent of police departments in the U.S. Thirty years later, LodeStar wants to create “a safer, reliable handgun that can only be fired by the authorized user.”

Without the programmed ID token nearby, the LodeStar personalized handgun is always in the “OFF” position. When the gun and the chip are within a few inches of each other, the firearm immediately lights up green — and the gun fires. Battery life lasts up to 10 years. And the LodeStar gun promises to be hacker-proof, unlike an early prototype by Armatix.

John Diaz, former Seattle police chief, said he much prefers LodeStar’s RFID (radio frequency ID) technology, the same used on a remote car lock. He believes RFID works better than biometric or fingerprint recognition.

“Officers wear gloves, they’re down in the mud, and biometric isn’t reliable,” said Diaz, also a board member at LodeStar. “Our officers in Seattle switched to Glocks about 20 years ago, and some new calibers about seven or eight years ago. If police officers are ever to move to smart guns, their acceptance comes down to reliability.”

Accidental gun deaths are another reason why smart guns make sense for law enforcement and consumer buyers, Glaser said. With RFID technology, “as soon as the token or bracelet is out of range, the gun stops working.”

Police officers could program their weapons to be fired by their partners, if necessary, but not by anyone else, he added. So could parents with children in the house.

Smart-gun technology could also help stem the flood of stolen guns and accidental deaths: roughly 38,000 Americans are fatally shot each year, and an additional 80,000 people in accidents and suicides. Since the year 2000, “more than two million people have been shot accidentally, and 500,000 have died, more than all military killed since the Civil War.”

Glaser worked in-house as an attorney for ExxonMobil and then Alcon, which went public. “I’m the business guy,” he said. Mauch, on the other hand, is considered weapons royalty, as is Jonathan Mossberg, of the Mossberg rifle maker family, who also advises LodeStar.

LodeStar’s advisers and investors are pinning their hopes on New Jersey, where State Senate Majority Leader Loretta Weinberg (D., Teaneck) and Gov. Murphy have pledged support for smart guns.

In 2002, New Jersey became the first state in the nation to enact a law requiring that all handguns sold in the state be childproof once the technology became available and approved by the state. Gun lobbyists pushed back and threatened store owners, prompting them to back off from selling smart firearms.

In 2017, the New Jersey Legislature tried to repeal the 2002 mandate and instead require each firearm retailer in New Jersey to sell a personalized handgun model once they are available. Then-Gov. Chris Christie vetoed the bill, but Murphy has signaled he will sign any new law.

In an interview, Weinberg said she expects the New Jersey mandate will be repealed and replaced this year under Murphy.

“We are all in agreement that the mandate to purchase should be rolled back, while also protecting retailers who want to offer a childproof handgun,” she said.

Mauch, for his part, said he was moved to create a smart gun after having to testify in the case of a 6-year-old California boy who shot his best friend with his father’s handgun.

“I had to explain to the judge why that pistol shot this poor boy. … How should a dumb piece of metal know who is using it? The pistol must function in the hands of a policeman or soldier with NO COMPROMISE and should not function in the hands of that young boy,” he wrote in an email from Germany, where he’s based.

But the technology didn’t exist then. That event “pushed me to make that kind of product,” Mauch said. “A pistol that only functions in the hands of the official owner to make sure that nobody else can use that instrument for misuse.”

There’s not a lot of income in fixed income these days, so active management of your bond portfolio is even more important, says Eaton Vance’s Kathleen Gaffney, one of Wall Street’s most astute fixed-income investors. So how are she and other active bond-fund managers generating returns?

During this week’s 70th annual CFA Institute conference, to be held Monday through Wednesday in Philadelphia, Gaffney, along with Vanguard founder John Bogle and Wharton School finance professor Jeremy Siegel, will share their thoughts on investment strategies in the current environment. (CFA, or chartered financial analyst, is considered to be one of the toughest designations to achieve. We lovingly refer to the CFA confab as a “nerdfest.”)

Eaton Vance Management’s Gaffney, a CFA charter holder, is codirector of investment-grade fixed income, and lead portfolio manager for Eaton Vance’s multisector bond strategies. She’s responsible for buy-and-sell decisions and portfolio construction. She joined Eaton Vance in 2012 after working for many years with Loomis Sayles bond guru Dan Fuss.

“It’s extremely hard to generate income now, and that’s exactly the time you don’t want to reach for yield,” Gaffney said. “That’s why active bond portfolio management becomes your most important defense in this frustrating environment.”

Sectors where yields – the income on a bond – are rising, she said, include retail companies, mall REITs, and telecommunications.

“The reason they yield so much is fundamentals are deteriorating, and investors are demanding more income. That can be a very tricky investment, because what’s the potential downside?”

Instead of Amazon or Apple, she buys bonds that have sold off sharply and offer value, such as Seagate Technology, a disk-drive manufacturer. “Seagate was a sleeper old-tech company that’s been through different cycles. We still need standard computer storage, and the more data out there, the more demand for Seagate.”

Gaffney bought the 10-year and the 30-year bonds when they were yielding 8 percent and trading around 70 cents on the dollar. “We’ve pared back,” she said, “because they’ve done very well.

“The great thing is, you have underlying asset value that minimizes the downside. To me, that total return is the way to manage fixed income,” meaning price appreciation plus a decent yield.

The Eaton Vance Multi-Sector Income Fund can hold a maximum of 35 percent of below-investment-grade bonds, as well as floating-rate bank loans and emerging-market dollar-pay corporate debt.

Interestingly, it doesn’t hold U.S. Treasuries.

“We don’t own them. The yields are low. Growth should pick up here in the U.S., but there’s tremendous uncertainty. The Fed can’t fix that, only politicians can.

“Today reminds me of the summer of 2014, as there doesn’t seem to be a lot of value. What’s different is the extremes we see in volatility,” particularly driven by politics in places such as Puerto Rico and Brazil.

“Politics are driving volatility, and the fact that expectations for economic growth and fiscal stimulus are now in doubt. I believe we will get there one way or another, but the election was tied to getting U.S. growth going,” she said, which has been sidetracked by recent White House turmoil.

Because short-term interest rates remain so low, “investors can’t earn money in the market, and yet we have this reach for yield, so every investment asset is overvalued or crowded.”

Gaffney believes bond investors plowing money into low-cost ETFs and index funds may beget disappointment because “everyone owns the same thing. When volatility picks up, a lot of funds have to reposition and sell. That can create a vicious negative feedback.”

As for Puerto Rico, “we expect a long-term workout, which is already priced into the bonds. We view the revenue bonds as more attractive.” Eaton Vance also owns Brazilian dollar-pay corporate bonds, as she believes Brazil is “turning the corner, but with a long path to where the country needs to be. Brazil is an excellent example of a country that benefited from investment-grade ratings.”

Gaffney holds such Brazilian corporate-bond names as energy giant Petrobras and JBS, a food manufacturer, which offer yields of 6.5 percent to 7.5 percent on bonds ranging from 10-year maturing in 2027 all the way out to 2043. Gaffney is also positioning for a turn in the U.S. dollar – which has been trading at a multiyear high against many currencies.

“We own the Brazilian government bonds, denominated in reals; Mexican government bonds, denominated in pesos; bonds payable in Indonesian rupiah and Indian rupees – these are countries on the path toward reforms. We’re likely to see their currencies benefit vs. the U.S. dollar,” she said.

“Our view is that the push for fiscal stimulus here means inflation, and nominal growth feels good if wages are moving up” at the same time.

Eaton Vance also expects that growth globally could lead to rising inflation in the United Kingdom, Germany, and China. “We’re likely to see a weaker yen, a stronger euro, and the U.S. dollar weaker relative to emerging markets,” Gaffney said.

Not surprisingly, Bogle will be talking about “the index revolution and what it means to professional investors, who are starting to think about asset allocation more and stock picking less. In some cases,

it’s gone too far. It used to be just stocks and bonds, and now it’s highly complex allocations based on data mining,” he said. “That’s not healthy.”

Given the flood of money into passive index funds, we asked Bogle: What happens if everyone invests using only index funds?

“There’s zero chance of that happening. Indexing represents 22 [percent] to 23 percent of the U.S. market. There’s just too much trading out there.”

For a list of CFA speakers, visit the conference website (annual.cfainstitute.org/speakers).

Some content on this page was disabled on June 11, 2020 as a result of a DMCA takedown notice from Philadelphia Inquirer. You can learn more about the DMCA here:

It’s the story of Lansdowne lawyer Robert Kempner, who until his death held on to a startling secret — he’d prosecuted Nazi officers at Nuremberg, and purloined the private diary of Hitler’s favorite ideologue Alfred Rosenberg.

But that is just the latest crime he’s solved. Wittman joined the FBI as a special agent in 1988, and was drawn to art crimes not longer after starting work at the federal agency. His mentor suggested taking art appreciation classes at the Barnes Foundation when it was still located on the Main Line.

As a result of that and other specialized training in art, antiques, jewelry and gem identification, he served as the FBI’s investigative expert involving cultural property crime. During his 20-year FBI career he helped recover more than $300 million worth of stolen art and cultural property.

Wittman, in 2005, created the FBI’s rapid deployment national Art Crime Team, and represented the U.S. conducting investigations and instructing international police and museums in recovering stolen works and in security techniques.

He retired in 2008. In 2010, Wittman penned his first book — The New York Times bestselling memoir “Priceless: How I Went Undercover to Rescue the World’s Stolen Treasures.” His second book, “The Devil’s Diary,” co-authored with journalist David Kinney, ranks also as a best seller, published in 26 languages in 30 countries.

Today, Wittman works for himself as president of Robert Wittman Inc., specializing in consulting on art matters, which include expert witness testimony, security, investigations and collection management. A Chester Springs resident, Wittman remains a huge fan of the Barnes collection — and believes the move into center city was the right one.

“I went through the Barnes training program in 1991. Then later, I worked with the then-directors of the Barnes on their security, because the windows in the old house weren’t even locked. The HV/AC needed upgrades, and the paintings needed conservation. [The collection] was made for the world, and it’s really put Philadelphia on the map.”

Wittman’s worked for clients such as the owner of a private library of 10,000 books, including first editions of Tom Sawyer, pages from an original Guttenberg bible, and manuscripts authored by Theodore Roosevelt.

“The collection hadn’t been looked at in 45 or 50 years, and we had to cut the locks off of steamer trunks just to take a look and form a complete list,” he recalls. After inventory, Wittman valued the collection “in the millions of dollars,” in part due to an original Shakespeare folio — itself worth six figures.

Spotting forgeries is the key part of Wittman’s business — as is establishing true provenance for a works of art, cars, antiques, sports memorabilia and militaria. Wittman estimates the total global art market at $200 billion — $80 billion of that in the U.S. Art crimes represent roughly $6 billion of the world total.

“Believe it or not, all four major U.S. sports markets total $26 billion and the art market $80 billion. We love our art.”

And it’s not just phony paintings he investigates. There are forged baseball cards, Confederate belt buckles, even fake replica Batmobiles. One of Wittman’s recent clients bought $300,000 worth of paintings on the Internet from a dozen or so galleries.

“We just found out the paintings were all fake. Like any investment vehicle, you have to check provenance,” or where and how the work was obtained, he warns.

When valuing art and collectibles, “it’s a three-legged stool: authenticity, legal title, and provenance. It helps to use an art advisor, and get promises of what you’re buying in writing first.”

Wittman grew up around collectors; his father and mother ran an Asian antiques store, and while they never made much money, he learned to love the trade. Favorites in his own collection? Japanese ceramics, Civil War relics, fine art prints like Miro and Dali, and some Asian art.

“My most expensive piece probably isn’t worth more than $2,000 or $3,000.”

What does he recommend for art lovers buying anything above that price?

“If you are buying art as an investment, I’d use an art advisor. Collectors in high value art want to show it off. There’s a lot of serious collectors in Philadelphia, because there’s still a lot of old money.”

Wittman still gets phone calls in the middle of the night when art thieves strike.

“I can do a lot more now that I’m not an FBI agent, because before I could only do criminal case. Now I can do civil work as well as testifying as an expert witness,” he says.

Recently, Wittman worked the case of a stolen piece of glass that was on display at the Philadelphia Museum of Art. Originally owned by the founding family of the Wistar Institute, the piece had been stolen in the 1980s, hoarded in a storage unit, then later sold to an art dealer in New York.

The dealer resold the glass to a buyer for tens of thousands of dollars and it was put on display under consignment at the PMA.

“It took a year, but we proved it was stolen from Wistar — and now the family own it again.”

The piece is still on display at the Philadelphia Museum of Art — but with the rightful owner on the label.

Pennsylvania is to set to issue regulations on legal medicinal marijuana, and senior support is at an all-time high.

According to the Centers for Disease Control’s National Survey on Drug Use and Health, seniors are the fastest-growing users of medical marijuana in the country.

The September study, among those who had tried marijuana in the last month, showed the 55-and-older crowd was the quickest-growing demographic in the years 2002 to 2014: The number between the ages of 55 and 64 who used marijuana grew 455 percent, and the number 65 and older grew 333 percent.

Dana Rohrabacher, a Republican congressman from California, used cannabis lotion for his arthritis, time-stamping seniors’ new affinity for medicinal marijuana products.

Rohrabacher tried a topical, wax-based marijuana treatment. That night was “the first time in a year and a half that I had a decent night’s sleep because the arthritis pain was gone,” Rohrabacher said last year.

Pennsylvania is about to issue new regulations on dispensing legal medicinal marijuana, and senior support is at an all-time high.

“More than half the country has legalized medical marijuana. Now, older people who used marijuana when they were younger, perhaps in college, then entered the professional world and had families and stopped using – now that it’s legal in their state, what we’re finding [is] they’re going back to it, trying it again for health and wellness,” said Chris Walsh, editorial director and founding editor of Marijuana Business Daily in Colorado.

“Medical marijuana is now mainstream. You can walk into a heavily regulated storefront dispensary, and that prompts more people to consider it a viable medical option,” Walsh added.

In particular, many new lotions, creams, and pills an older person might use are heavy on a compound called CBD – cannabidiol, the painkiller – as opposed to THC, the chemical that gets you high.

Older people prefer traditional forms of medication, fueling growth in the industry, said Nick Kovacevich, co-founder and CEO of Kush Bottles, a medical marijuana packaging company.

“The ways you can ingest are changing. For instance, a 60-year-old might not be into smoking,” Kovacevich said. “Now, in many states, you can get pills, topicals or tinctures that you put under the tongue. Even in the last four years, the forms you can take have evolved into edibles like gummies, hot chocolate, lollipops, and lozenges.”

Heavier users, such as cancer patients, often prefer waxes or oils, skin patches, sublingual strips, creams, sprays, and lotions.

“That’s the wave of the future. The elderly like creams and sprays and rubs, because they’re used to ointments and gels for pain management and control,” Kovacevich said.

Conditions among the elderly that are listed as uses for medical marijuana include glaucoma, post-traumatic stress disorder, spasms, epilepsy, chronic pain, backaches, multiple sclerosis, and Parkinson’s.

Seniors campaigning for wider uses include Robert Platshorn, 73, who was born in South Philadelphia, grew up in Cherry Hill, and now lives in Florida.

“There are millions of junkie seniors taking OxyContin, fentanyl, and Darvocet,” said Platshorn, who founded TheSilverTour.org, an nonprofit and activist group of seniors lobbying for passage of medical marijuana in Florida.

“It’s a natural for physicians to prescribe medical marijuana for seniors who are in pain but who don’t want to feel loopy. And opioid addiction can be avoided,” he added.

New studies point to medical marijuana as a possible treatment for Alzheimer’s.

Gary L. Wenk, a professor of psychology, neuroscience, and molecular virology, immunology, and medical genetics at the Ohio State University and Medical Center, studies chronic brain inflammation in Alzheimer’s disease. His research into cannabinoids led him to conclude that while they are no cure, they may slow the onset of Alzheimer’s.

“Low doses of marijuana for prolonged periods of time at some point in your life, possibly when you’re middle-aged to late middle-aged, is probably going to slow the onset or development of dementia, to the point where you’ll most likely die of old age before you get Alzheimer’s,” Wenk said in a 2014 interview with Leaf Science, a Canadian marijuana-news website.

Even Philadelphia’s medical schools are getting in on the research of medical marijuana. In May, the Institute of Emerging Health Professions at Thomas Jefferson University announced the creation of the Center for Medical Cannabis Education & Research, which provides information and guidance to clinicians and patients about the medical uses of marijuana and cannabinoid-focused therapies.

With legalization, Platshorn argued, seniors “need to be part of the conversation surrounding legalizing medical marijuana, and its benefits.”

Laura Katz Olson taught health-care policy for decades at Lehigh University and could rattle off the ins and outs of Medicare and Social Security.

Laura Katz Olson, a Lehigh University professor and author of “Elder Care Journey,” says: “I had a lot of ideas on paper. They didn´t seem real until I experienced them myself.”

But none of that prepared her for caring for her mother, Dorothy Katz, a Senior Olympics medal winner who developed Parkinson’s disease.

Thrust into a long-distance caregiving role, Olson, 71, began grueling travel between Pennsylvania and Florida. Her mother’s health failed with each passing visit.

“At first, I was convinced she could ‘age in place,’ as they say,” Olson said. After her mother fell, then nearly died in a rehab facility, Olson moved her to Pennsylvania.

What Olson discovered in assisting her frail parent was at odds with her work as an elder-care expert. She could barely navigate the byzantine web of public and private insurance and services.

“As an academic, I looked for statistics and percentages on how Medicaid affects people. I had a lot of ideas on paper,” she recalled with a rueful laugh. “They didn’t seem real until I experienced them myself.”

Olson’s two siblings had died, so her mother’s care fell to her entirely. Her work teaching at Lehigh was interrupted as Dottie Katz steadily grew incapacitated by Parkinson’s-related dementia and a gradual loss of vision.

“You can only get your parent 10 hours of in-home care a week under Medicaid. Then the gap in service becomes real. I had to fill in the gap myself,” Olson said of her visits to Florida.

“While everyone is pushing for at-home care, there’s not enough coverage under Medicaid. In order to be eligible, you have to be nursing-home eligible,” which means your elder relative’s assets have been depleted.

In 2013, she moved her mother, now 93, into Gracedale, a county-run and subsidized senior facility in Nazareth, Pa.

Finding a facility for her mother and ensuring that her benefits stayed consistent shattered Olson’s convictions and exposed irrationalities in government systems. Despite her expertise, Olson was ill-prepared to deal with the bureaucratic barriers imposed at every turn.

“I was surprised at how much every service is siloed,” she said. “It’s so burdensome as to be impossible. The VA? To deal with them [Dottie Katz’s husband was a veteran] is a nightmare.”

In Pennsylvania, the Department of Human Services threatened to cut off her mother’s benefits because of one missing piece of paper – a bank statement that Olson had already submitted. “They just wanted paperwork again and again, to reinvent the wheel at every agency,” she said.

Another office threatened to stop her mother’s Medicare.

“The paperwork, the constant paperwork, that was surprising. And she has to reapply every year for Medicaid, which is a program for the poor.”

As with any program for the poor, Olson said, “the agency assumes you’re stealing and trying to get something for nothing. You have to prove everything – even if you’re 93, blind, and have Parkinson’s! The sting of it was unfathomable.”

Olson’s new book, Elder Care Journey, speaks to elders with functional limitations and the adult children helping them. The book documents the stresses and the manifold indignities in dealing with social-welfare agencies. Elders with limited financial resources often must rely on government funds for their basic care.

“I wanted to elucidate the obstacles confronted by other families attempting to navigate the complex and sorely inadequate programs serving the low-income aged,” Olson said.

At Gracedale, Olson said, she has found a place providing decent care, so she no longer fears for her mother’s health, safety, and well-being.

After reading her story, she said, “people coping with elder-care responsibilities should feel less alone in their struggles.”

Along the way, Olson discovered that many nursing homes and elder-care facilities are owned by private equity firms or multichain conglomerates traded on public exchanges. “Their primary profit goals are at odds with the well-being of the people they are supposed to be serving.

“I wrote this book as catharsis, then I realized my experience isn’t unique. There are serious issues with our long-term-care system. We spend billions of dollars of our federal and state budgets on long-term care and aging, and why aren’t we getting better results?”

Almost half of private nursing-home revenue, 48 percent, comes from Medicaid and Medicare. About 80 percent of all home-care agency revenue also comes from those sources, said Ron Barth, CEO of LeadingAge, a consortium of nonprofits in the elder-care industry.

“The taxpayers are funding the long-term industries but aren’t getting quality of care for their elders,” Olson said.

She visits her mother every day and advocates for her.

Is that necessary?

“Yes, because I know the aides are overworked, underpaid, and overwhelmed. And even the best of them can’t do it, because they have too many patients.”

Remember when Mom and Dad bailed you out on that overdue bill?

Now, it may be your turn.

More than half of U.S. states have so-called “filial responsibility” laws that require adult children to support their parents if they become indigent.

For example, under Pennsylvania’s 2005 statute, spouses, parents, and children are obligated to care for or financially assist destitute family members.

That means you could be held financially responsible for a parent’s nursing-home care, says Marc Jaffe, estate-planning lawyer and partner at Fromhold Jaffe & Adams in Villanova, Pa.

“A nursing home will sue an adult child to recover monies the parent didn’t pay,” Jaffe says.

“It’s not used very often. And you are not necessarily responsible for all of that person’s debts. However, you might be held responsible for that person’s food, shelter, clothing, medical care, and other similar necessities if the person did not have the funds to pay,” he notes.

Such lawsuits “may become more common, as the government in general is looking to be less generous with benefits, and if a medical provider doesn’t get paid, they may look more toward the family,” Jaffe adds.

A 2012 Pennsylvania Superior Court case, Health Care & Retirement Corp. of America v. Pittas, made it clear that under state law, if a creditor chooses, one child alone may be found completely responsible. The court upheld the nursing home’s judgment against one son for $92,000 for his mother’s care after she left the facility and moved to Greece.

The Superior Court also determined what is meant by indigent. It includes not only those who are completely destitute and helpless but also those people who have limited, but not sufficient, means to support themselves financially.

Pennsylvania, New Jersey and Delaware all have similar “filial responsibility” laws on the books – although, again, they are rarely enforced, says Trisha Hall, partner with Connolly Gallagher in Wilmington.

In recent years, the Pennsylvania Bar Association supported a repeal of that state’s law, but it was blocked by the Department of Human Services and nursing-home lobbies, says Katherine Pearson, a professor of law at Pennsylvania State University’s Dickinson School of Law in Carlisle, Pa.

In January 2015, House Bill 242 was proposed by State Rep. Anthony DeLuca (D., Allegheny), who wrote that “current law gives the Department of Human Services authority to go after adult children to collect money for indigent parents’ care. This law is not only outdated and impractical, but it also has vast potential for abuse and to unfairly cause serious harm.”

Seldom enforced

Most of these laws are seldom enforced because federal law prevents the states from considering the financial responsibility of any individual other than a spouse in determining the eligibility of an applicant or recipient of Medicaid or other poverty programs, Pearson says.

But Pennsylvania also has little incentive to change the law.

“The state wants the statute to stand as a way to offset state liability” for indigent elderly, she adds.

What is unique about Pennsylvania is that the law has been interpreted as permitting third parties, such as nursing homes, to sue the children directly, Pearson explains.

She has been watching cases in which nursing homes are suing adult children for bills as low as $5,000 or as high as $60,000.

“Sometimes, these bills have accumulated, and then they sue the adult children retroactively – as a debt-collection tool.”

To protect themselves, Jaffe advises that adult children put their assets in protective trusts or retirement accounts, which cannot be claimed by creditors, and that they put property in joint ownership, under more than one name.

Better communication

In some cases, families could solve financial and other problems ahead of time simply by having conversations about what their elderly parents want.

“Four in 10 families don’t agree on the roles adult kids will play” as caregivers, says Suzanne Schmitt, vice president of family engagement at Fidelity Investments, based in Boston, Mass.

Start small, Schmitt advises, asking your parents where their important documents are, such as their health-care proxies and HIPAA release forms, among others. “Keep it tactical and don’t tackle the whole conversation at once.”

Don’t ask, “How much have you saved?” Instead, ask general questions, such as, “Where are your bank and savings accounts held? Do you have a trusted adviser such as an estate-planning attorney or CPA?”

Schmitt herself has had the conversation with her parents. And many elderly parents will appreciate bringing up the subject – and are encouraged to do so when families get together for holidays and other occasions.

“It’s tough,” she says, “but I started with saying I wanted to honor their wishes and not guess about what they wanted.”

How much money do public companies spend on politicians, and what do they disclose?

An index offers a peek at the juicy details.

For the first time, the 2015 CPA-Zicklin Index gives a breakdown of every company in the S&P 500: which policies each company maintains on political contributions; if the company even has a policy; and links to how much moolah it donates.

The index, started in 2009, shows the largest publicly held U.S. companies’ political activity in a high-spending era marked by an unprecedented flood of dark money, said Bruce Freed, president of the Center for Political Accountability in Washington, which partnered with the Wharton School of the University of Pennsylvania to create CPA-Zicklin.

For investors, it’s a useful tool to evaluate companies’ policies and accountability.

For companies, it helps “assess whether they follow best practices for disclosure and accountability, and the extent to which they demonstrate commitment to these principles,” Freed added.

The local communications giant Comcast, for instance, scored high on the CPA-Zicklin Index for transparency and for having a stated policy on political contributions. On its corporate website, Comcast posts a 59-page document listing donations totaling $6.5 million made in the most recent 2014 election cycle.

“Comcast’s political contributions are made from employee-funded political action committees (‘PACs’) that are sponsored by Comcast. The Comcast PACs are operated by a board of directors, chaired by the senior executive vice president. When permitted by law, political contributions are also made out of corporate funds,” the company said on its website.

Comcast’s largest 2014 donations included $367,000 to the Republican Party of Florida, $250,000 to the Democratic Governors Association, and $255,000 to the Republican Governors Association.

In Pennsylvania, Comcast donated mostly to individual candidates, including $50,000 to Tom Wolf for Governor, $10,000 to Bob Brady for Congress, $17,000 to Friends of Dominic Pileggi, $15,000 to Friends of Joe Scarnati, and $16,000 to the Mike Turzai Leadership Fund.

How did the CPA-Zicklin Index come into being?

Lawrence Zicklin, a former partner at the Wall Street firm Neuberger Berman, funded the Zicklin Center for Business Ethics Research at the Wharton School. (He currently teaches ethics at Wharton and several other business schools.)

William Laufer, director of the Zicklin Center, first proposed the index in July 2009.

In the 2015 index, three companies tied for a first-place rating of 97.1 points out of 100: Becton Dickinson; CSX Corp.; and Noble Energy.

Among regional companies, Comcast scored 81.4; AmerisourceBergen scored 82, and Hershey Co. scored 90. Those with low scores included Lincoln National (17.1), PNC Financial Services (5.7), and Urban Outfitters (0.0).

The average overall score in 2015 was 72.6 for companies with some sort of disclosure agreement.

“Companies engaged by shareholders, and reaching an agreement, had significantly better disclosure and accountability policies,” he said.

More than half the S&P 500 – 52 percent, or 259 companies – had detailed policies on campaign donations. Thirty-five percent, or 176 companies, had brief or vague policies.

The majority of S&P 500 companies – 54 percent, or 270 companies – had dedicated webpages to address political spending.

Zicklin said he became interested in campaign finance nearly a decade ago, when Massey Energy CEO Don Blankenship donated $3 million to a West Virginia judge who later decided a case in the company’s favor.

“I’ve also heard from many companies that they would like to get out of this game if they could,” Zicklin said. “In some cases, companies are being extorted. They’re told there’s a bill they really ought to support by some nameless politician, and they have to [donate].”

More important, he said, “Americans are very upset. They feel they have no part in how government is run – it’s all by big checkbooks.

“I can’t change Citizens United,” the Supreme Court decision on political donations by companies, “but I can at least make it transparent.”

We’re getting a crack at new technology: a retirement plan robo-adviser.

My colleagues and I have a 401(k) administered by Vanguard, the local mutual-fund giant. A few weeks ago, we got letters in the mail saying we’re eligible to try out Financial Engines’ “Retirement Evaluation” tool free for a few months.

If we sign on – and I’m going to road-test it – Vanguard charges 0.40 percent annually, more expensive than just indexing. (Currently, I have my Vanguard savings in one low-cost index fund). I’m not crazy about the extra fee, because it seems antithetical to Vanguard, but personal advice costs money.

Vanguard clients’ uptake on the Financial Engines tool has been so-so (about 7 percent of all plan participants), but I’m willing to see what the tool suggests.

The evaluation includes a phone call, if desired, to go over other assets such as Roth IRAs, annuities, and the like.

I’ll report back with results from Vanguard and Financial Engines in a few weeks. They’re crunching my measly portfolio to see whether I’m on the right track, style-wise.

If I don’t like the advice, I can quit the service before the deadline and pay nothing.

We’re probably late to the robo-adviser party – Financial Engines partnered with Vanguard in 2001.

Like Vanguard, Financial Engines is a quiet giant. Founded in the 1990s, it boasted $104 billion under management in January, compared with $88 billion in January 2015 – an increase of 18 percent.

Vanguard’s own hybrid robo-adviser, Personal Advisor Services, had $31 billion in January 2016. (It launched in 2015.)

Rivals include Charles Schwab’s Intelligent Portfolios, launched in 2015. As of January, Schwab’s robo-adviser assets stood at $5.3 billion.

Vanguard remains the juggernaut, attracting almost $29 billion to long-term mutual funds and exchange-traded funds as of March – more than all competitors combined, according to Morningstar. Having built its reputation on low fees, Vanguard was the leader in estimated flows to both actively managed funds as well as those that track indexes.

The shift toward passive investing has accelerated in bonds, too. Vanguard’s collections in March represented 59 percent of the money the entire industry gathered during the month.

BlackRock’s iShares unit attracted almost $15 billion to its ETFs. Losing firms included PIMCO and Franklin Resources, with net redemptions during the month, according to Morningstar.

The Securities and Exchange Commission has a relatively new cop on the beat here: Sharon Binger, director of the Philadelphia Regional Office.

The Philly office oversees enforcement and examinations for the mid-Atlantic region. Binger joined it from the SEC’s New York office in 2014, where she was assistant regional director.

Sharon Binger became director of the Philadelphia regional office in 2014, after working in New York.

In an interview, Binger outlined some recent cases and priorities, first highlighting the one filed last week against Paul-Ellis Investment Associates, which the SEC examined at the firm’s offices at 1818 Market St.

In a suit filed against Joseph Andrew Paul and John Dee Ellis Jr., both of Philadelphia, the SEC alleges that the men orchestrated a fraud of a dozen retirees that totaled $3.9 million.

From 2010 through December 2012, the SEC’s suit says, Paul and Ellis raised the money through free-dinner seminars at which they promised double- and triple-digit returns annually. One Paul-Ellis employee claimed the investment strategy was “performing as expected in the 2 percent-4 percent weekly range.”

“These kinds of cases are our bread and butter, which is investor protection,” Binger said.

“It’s important to understand who you’re investing with, and we have resources to consult before you invest your money,” she said.

The fact that an investment firm is registered with the SEC “provides investors with more transparency,” she added.

Paul and Ellis marketed themselves as experienced money managers with a phone track record, a prospectus, and some glossy marketing materials to supplement the free meal.

Yet just a few minutes on the FINRA (Financial Industry Regulatory Authority) and SEC databases reveal that Paul had multiple disciplinary incidents and fines years before the recent case.

Ellis also was a registered representative with a disciplinary record.

By July 12, 2012, Paul-Ellis investors’ funds were gone, the SEC suit says, and it notes that an investigation showed the two spent the money.

I tried reaching their office in Center City, and the number no longer works.

“When we are promised returns that are too good to be true, we may have a tendency to suspend common sense,” Binger said.

The SEC exam team went to Paul-Ellis “to make sure they were following the rules. They identified areas of concern and referred it to enforcement,” she said.

To track insider trading, Binger’s team uses technology.

In January, it won a verdict in a U.S. District Court trial in Philadelphia against Nan Huang, charged with insider trading on information obtained from his employer, Capital One Financial.

Huang and another defendant searched Capital One’s credit-card activity for millions of customers at corporations. He then traded in advance of the public release of those companies’ quarterly sales.

Binger is proud of her office’s ability to freeze assets quickly, including in cases where defendants may flee the country, as Huang did, flying to China.

“We’ve gotten asset freezes in a number of cases, including the Huang case and in the hacking case” by accused insider trader Vitaly Korchevsky and 41 others, she said.

Last year, Korchevsky was indicted on charges that he helped orchestrate an insider-trading scheme regulators said netted $100 million. He was arrested by the FBI at his Glen Mills home as part of a group that tapped corporate press releases before they became public.

“There’s the concern the money will go quickly,” Binger said. “In the Huang case, one defendant fled the country shortly before we filed our lawsuit, and the other fled the day after. We were fortunate to freeze more than $1.6 million before it left the country.”

If you have questions or concerns about your broker or money manager, you can contact the local SEC office by email at philadelphia@sec.gov.

Or you can call the SEC’s Office of Investor Education and Advocacy at 1-800-732-0330. Additional contact information can be found at http://www.investor.gov/contact-us.

Ken Springer, a former FBI agent, runs a firm called Corporate Resolutions that educates high-net-worth clients, including professional athletes and doctors.

“It’s like wearing a seat belt. You need to vet your investment manager,” Springer says. “Look at what these people did in the past, at the track record, and ask other investors if they’ve done background checks and gotten referrals.”

Tax filer: Don’t worry if you get a phone call, a text, or an email from the Internal Revenue Service.

It’s not the IRS. It’s a scam artist.

This year, the criminals are putting a new twist on an old script. They call saying they already have your tax return and just need to verify details to process your refund.

The scammers try to convince you to give up personal information such as Social Security number, driver’s license details, bank account numbers, or credit-card numbers.

Hang up the phone. Don’t click on that email. The days of giving out information unsolicited are over.

“These schemes continue to adapt and evolve in an attempt to catch people off guard just as they are preparing their tax returns,” IRS Commissioner John Koskinen said in a statement last week.

“Don’t be fooled. The IRS won’t be calling you out of the blue asking you to verify your personal tax information or aggressively threatening you to make an immediate payment.”

Scammers claiming to be IRS officials may demand that you pay a bogus tax bill by sending cash, usually through a prepaid debit card or wire transfer. They may leave “urgent” messages by phone or via email.

They may politely ask you, the taxpayer, to verify your identity over the phone. They may try to bully or intimidate you. They may even threaten to arrest or deport you or revoke your driver’s license if they don’t get money.

One reader said he’d been called by someone claiming to be an IRS agent who demanded that they meet in the parking lot of a local Walmart to exchange cash.

Often, scammers alter caller IDs to make it look as if the IRS or another agency is calling. They may use IRS titles and fake badge numbers to appear legitimate. They may even have your name and address to make the call sound official.

To repeat: The IRS will never:

Call to demand immediate payment over the phone, nor will the agency call about taxes owed without first having mailed you several bills.

Call or email you to verify your identity by asking for personal and financial information.

Demand that you pay taxes without giving you the opportunity to question or appeal the amount owed.

Require you to use a specific payment method for your taxes, such as a prepaid debit card.

Ask for credit- or debit-card numbers over the phone or email.

Threaten to immediately bring in local police or other law-enforcement groups if you don’t pay.

If you get a phone call from someone claiming to be from the IRS and asking for money or to verify your identity, do not give out any information. Hang up immediately.

Contact the Treasury Inspector General for Tax Administration to report the call. Use the “IRS Impersonation Scam Reporting” webpage (www.treasury.gov/tigta) or call 1-800-366-4484. If you know you owe on your taxes, or think you owe, call the IRS at 1-800-829-1040. Tax planners and accountants confirm that scammers are hard at work this tax season.

“I have had four clients call me since the beginning of the year with IRS scams, and I’m sure there are more who just ignored them, as I told them,” said Mary Lew Kehm, certified public accountant in Whitehall Township.

“Their script now attempts to validate, as oppose to threaten,” said Michael A. Gillen, director of the tax accounting group at Duane Morris law firm in Center City.

Miller founded PACT for Animals, a nonprofit that finds foster homes for pets of service members and more. His next project will pair animals with retirement-community residents.

Miller, 74, retired as a lawyer and businessman and founded PACT for Animals, a Montgomery County, Pennsylvania nonprofit that will find a foster home for your pet.

PACT for Animals matches your companion animal with a foster family if you are heading off to serve in the military, have a long-term health crisis, or enter a hospital. And it’s free.

Miller’s next animal adventure? Working with retirement communities whose residents, he says, “would be perfect to serve as fosters for animals.”

“People over 55 are perfect: They’re settled, they probably don’t want to raise animals for another 20 years, but they can handle short-term companionship. And they don’t have kids.”

A West Philadelphia native, Miller graduated from the Wharton School of the University of Pennsylvania and University of Pennsylvania Law School, then received a master’s degree in tax law.

In the 1970s, he was a swinging single lawyer who didn’t want to settle down – until he met his girlfriend’s dog.

Then everything changed.

When they split, Miller gave the ex-girlfriend his car and “bribed” her two sons with a television and a motorcycle. Miller kept the canine.

“That’s when I learned about the human- animal bond,” he remembers.

By 2007, Miller had married and made enough money to retire. He and his wife, Judi, opened a retail pet store on the Main Line, Buzzy’s BowWowMeow, specializing in free adoptions of shelter dogs and cats.

Ultimately, they sold the Narberth business to focus fully on nonprofit work. (Buzzy’s is now a Doggie Style store.) In 2010, they formed the nonprofit PACT for Animals, part of which stands for People + Animals = Companions Together (pactforanimals.org).

The inspiration: A friend of Miller’s elderly mother adopted a mixed breed named CiCi headed for euthanasia. The woman had just lost her husband, and her daughter had cancer.

“That little miracle dog made her life worth living, turned her mental state around completely. CiCi showered her with unconditional love during her time of profound grief,” he says.

Today, PACT for Animals offers assistance all over the country.

“People drive and fly their companion animals from as far as California, Texas, Florida, and Idaho,” Miller says, in order for their pets to be placed in PACT’s more than 150 approved foster homes in the Philadelphia area.

Foster families sign a contract promising good care; PACT pays expenses and veterinary bills.

Foster parents are “usually middle-class people. They aren’t the people who live around here in Gladwyne,” Miller says, laughing, in the basement of his house – PACT’s offices – with his employees, many of whom are undergraduates at Bryn Mawr College.

“Every home in this neighborhood is worth a million bucks – all of them could take a healthy animal. But people with money rarely volunteer to foster our dogs and cats.

“But,” he adds with a wink, “they can write checks.”

By 2015, PACT had doubled in size: number of animals fostered, to more than 300; paid employees, four; volunteers, more than 45, who check foster-home quality and take pictures of the animals to send to their humans.

Miller and his wife live in an expansive house with a parrot, several cats, and a few dogs. Recently, Miller and his wife felt the pain of losing Chloe, one of their favorite dogs.

“Chloe was by my side for the last 10 years. Her love and cheerfulness sustained me on a daily basis through a world which gets uglier, sadder and more superficial,” he says.

“She was my rock through daily heartaches. I learned years ago never walk out of your front door without telling all those you love, both two- and four-legged, how much you care for them. It reminded me that the sudden loss of a loved one can occur any time,” Miller says, with tears in his eyes.

In the fourth quarter of his life, Miller knows he’s more interested in helping other people and their animal companions than in “chasing such goals as big money and power, which I sometimes was driven by in my legal and business career.”

PACT became a national organization faster than Miller anticipated.

“We are the only group really solving this problem with each family, each foster, and with each companion animal we save,” he says.

Today, he and his wife want for nothing material, he says.

“That gives me the freedom to continue my life’s mission – the human-animal bond. I am at an age when so many of my friends are leaving. The time to do my most important work is now.”

Roughly 15 years ago, I wrote an article about a notable Wall Street figure and his secretive investment fund that never, ever lost money.

His name was Bernard Madoff.

The dot.com bubble had just burst, yet Madoff’s hedge fund earned 10 percent that year, without missing a beat.

In May 2001, I wrote about some red flags surrounding Madoff’s hedge fund: eerily consistent returns and no losing years even when the stock market crashed, no due diligence allowed by investors, no independent brokerage statements, and odd threats that investors could not return to the fund once they had cashed out.

Madoff himself gave me a brief interview by phone, then metaphorically patted me on the head and told me to go away.

(At the time, I was a writer for Barron’s magazine, a must-read for Wall Street types.)

For a look into Madoff’s sociopathic mind, tune in to the ABC prime-time mini-series Madoff, airing Feb. 3 and 4 (8-10 p.m.).

Academy Award-winning actor Richard Dreyfuss stars as Madoff, with Blythe Danner as his wife, Ruth. Madoff follows the decades-long rise of the former investment guru and NASDAQ chairman, and his abrupt demise in 2008.

Best part of the show? Real investors, including Philadelphia-area locals Michael DeVita and his mother, Emma, talking about the devastating effect that Madoff’s epic lie had on their lives.

No one, including me, knew Madoff was running a classic Ponzi scheme – paying off old investors with money from new investors – to the tune of $65 billion. His theft is considered the largest financial scam in U.S. history, and the impact was global. Vaporizing billions of dollars worldwide, including the funds of philanthropies, charities, celebrities, and ordinary mom-and-pop retirement portfolios, Madoff used some simple con-man magic tricks to pull off a monumental fraud.

For those unfamiliar with the scheme, Madoff’s fund never invested a single dollar in the markets (emphasis mine).

Instead, the money sat in a checking account at JPMorgan Chase. Madoff and his crew of flunkies never made a single real trade. Instead, they created profits out of thin air, then printed and mailed out phony paper statements to clients every month, starting in the 1970s.

Among those who helped perpetuate the decades-long crime were right-hand man Frank DiPascali Jr. (played by Michael Rispoli), assistant Annette BonGiorno, two computer programmers, and clerical workers with high school degrees.

Frank Whaley plays skeptical competitor and whistle-blower Harry Markopolos, whose boss could not understand how Madoff kept churning out double-digit returns.

Markopolos warned regulators for years that Madoff was a fraud, and he ultimately testified before Congress about the SEC’s failings. (Harry’s best line in testimony: “The SEC couldn’t find their ass with their own two hands.”)

The mini-series also features Charles Grodin as Carl Shapiro, one of Madoff’s longtime investors, who was forced to return millions. Jeffrey Picower, the largest investor, returned $7 billion.

Picower and other billionaires were complicit in Madoff’s scheme, as I detailed in a subsequent book, Too Good To Be True (Penguin 2009).

Linda Berman and Joe Pichirallo produced the ABC film, and I spoke with Pichirallo last year about a few details to include. I’m no film critic, but Dreyfuss inhabits the role to a scary degree.

What’s missing? Any remorse or guilt on the part of the family, and the roughly $300 million in salary, bonuses, and properties that the Madoff family ripped off for themselves. The properties, including son Mark’s mansion in Connecticut, son Andrew’s apartment in Manhattan, multiple boats, and the beach house in Montauk, N.Y. , were later auctioned off to repay investors.

Others I won’t forget: the woman at Madoff’s sentencing who resorted to Dumpster-diving for food, and Nobel Prize-winning author and Holocaust survivor Elie Wiesel, whose foundation lost $15 million to Madoff. Incredibly, Wiesel said afterward: “We have seen worse.”

And the DeVitas, of Chalfont. Emma, now 88, and her son opened accounts with Madoff in the early 1990s, believing the fund was a retirement savings opportunity.

On Dec. 11, 2008, Madoff was arrested. The DeVitas’ life savings vanished.

“We did nothing wrong other than listening to the agency that is tasked by Congress with protecting me against this type of fraud,” Emma DeVita told me. “The Securities and Exchange Commission failed me.”

That’s the final missing piece from the ABC series. It’s up to us not to fall for more Madoffs and to do our own due diligence. We can’t count on the regulators to catch them first.

Beneficial Bequest

DECEMBER 20, 2015 Ridgely Bolgiano, a 1959 graduate of Haverford College, left the school $6.5 million. He he was able to increase both his retirement income and the amount he left the college.

With a net worth approaching $25 million, Ridgely “Ridge” Bolgiano this year left his alma mater, Haverford College, a $6.5 million gift using a relatively obscure form of retirement savings and philanthropy that benefits both the charity and the donor while he’s still living.

The vehicle in question – a charitable gift annuity – increased both Bolgiano’s retirement income and the amount he left the college.

And they aren’t just for the wealthy – the rest of us can use them, too.

Bolgiano graduated from Haverford in 1959 and, until his death at age 82 on Oct. 3, he lived in Gladwyne, Pa. A confirmed bachelor, he had no spouse or children.

He was an inventor and technology millionaire who made his fortune with InterDigital in King of Prussia, Pa. He was a physicist who owned more than two dozen patents, one of which is central to our everyday lives, the means by which a cellphone signal is transferred from cell to cell in a service provider’s network.

As he approached retirement, Bolgiano set up a “deferred” charitable gift annuity.

Such annuities are relatively unknown because banks, stockbrokers and financial planners don’t sell them. Only 501(c)(3) charitable organizations can offer them, according to Chris Mills, a spokesman for Haverford College.

Eileen Heisman, president and CEO of the National Philanthropic Trust, calls charitable gift annuities “great giving vehicles.”

They are complex on the inside, but fairly easy to set up.